IS YOUR HOME AN ASSET OR A LIABILITY? THE REAL ESTATE TRUTH

by: Remie Longbrake | published: February 22, 2026

You’ve probably heard it a million times: “Your home is your biggest asset.”

But here’s a question that might keep you up at night: If your home takes money out of your pocket every single month, is it really an asset? Or is it actually a liability dressed up in nice landscaping and fresh paint?

Let’s talk about the real estate truth that most people don’t want to hear.

The Question Everyone Should Ask

Does your home put money in your pocket or take it out?

That’s it. That’s the question.

Most people never ask this question. They just assume that because they own a home, they’re building wealth. They think homeownership automatically equals financial success.

But the reality is more complicated than that.

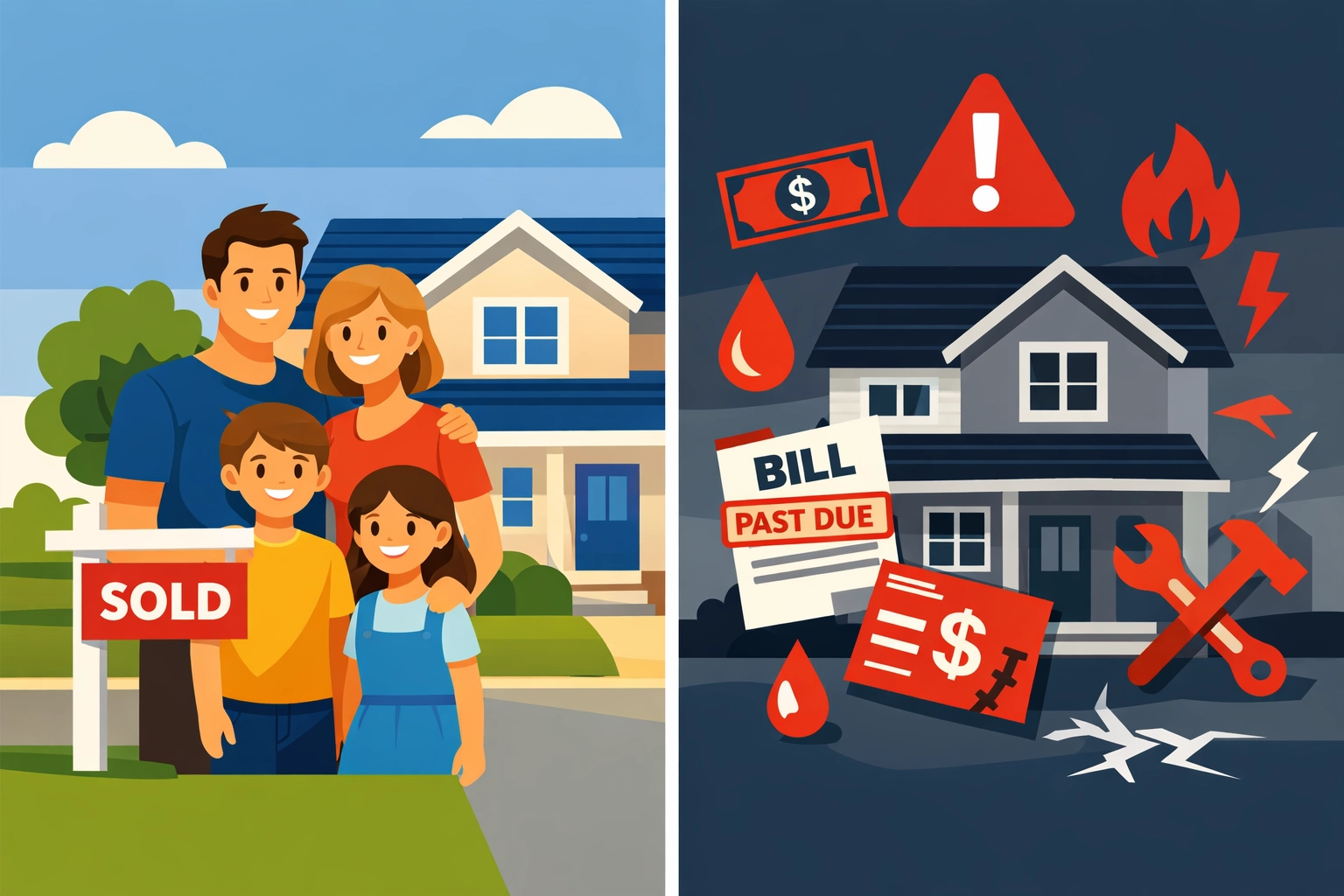

The Liability Side: Where Your Money Goes Every Month

Let’s start with the hard truth. Your primary residence costs you money every single month.

Here’s where your money goes:

Mortgage payments. Unless you own your home outright, you’re writing a check every month. A big chunk of that payment goes to interest, especially in the early years.

Property taxes. These never go away. Even after you pay off your mortgage, you’ll still owe property taxes every year.

Homeowners insurance. You need it. You can’t skip it. And it’s not getting cheaper.

Maintenance and repairs. Roofs leak. Water heaters break. HVAC systems need replacing. The rule of thumb is to budget 1-2% of your home’s value every year for maintenance.

Utilities. Heat, electricity, water, trash collection. These bills arrive like clockwork.

Add it all up. That’s a lot of money flowing out of your bank account every single month.

If you stopped working tomorrow, your house wouldn’t pay you. It would still demand a check. That’s the definition of a liability in the cash flow world.

The Asset Side: Where the Value Lives

Now let’s look at the other side of the coin.

Your home does have value. Real value.

Equity builds over time. Every mortgage payment you make increases your ownership stake in the property. Year after year, you own more and owe less.

Appreciation happens. In most markets, home values increase over time. Not every year, and not in every neighborhood, but the long-term trend is upward.

Tax advantages exist. Mortgage interest and property taxes can be deductible. There are tax benefits when you sell your primary residence too.

Forced savings account. Your mortgage payment forces you to build equity. It’s like a savings plan you can’t skip.

Inflation hedge. As the cost of living goes up, so does your home’s value. Your mortgage payment stays the same, but your home is worth more.

By the traditional accounting definition, your home is absolutely an asset. It has value. You can sell it. You can borrow against it.

So Which Is It Really?

Here’s the truth: It depends on how you look at it.

If you use the accounting definition, your home is an asset. It has value on paper.

If you use the cash flow definition, your home is a liability. It takes money out of your pocket every month.

Both perspectives are correct. They’re just measuring different things.

The accounting view looks at your net worth. The cash flow view looks at your monthly budget.

Most people need to understand both perspectives. Your home builds long-term wealth while costing you short-term cash. That’s the reality.

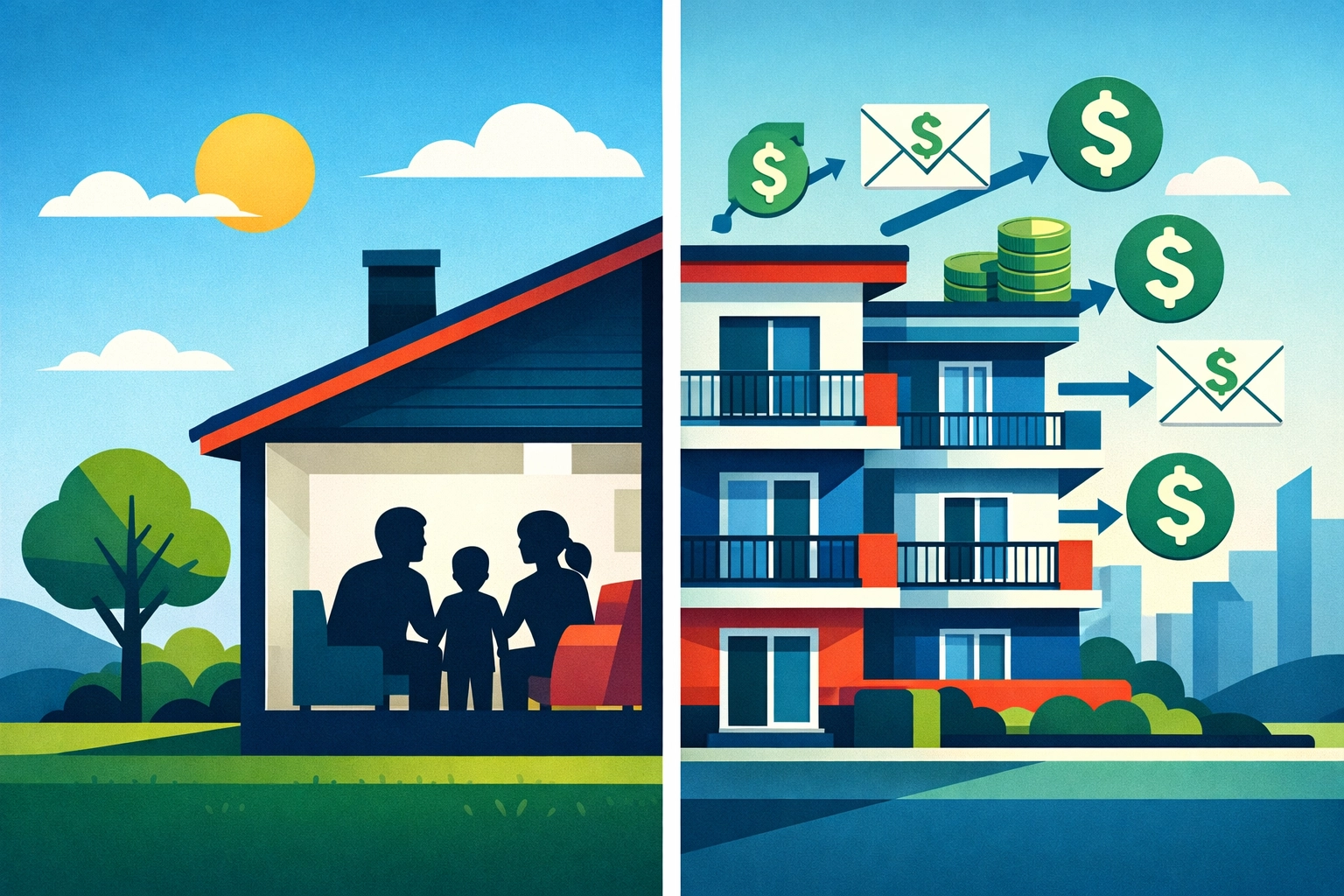

The Shift: From Homeowner to Real Estate Investor

Here’s where things get interesting.

What if you could turn your real estate from a liability into a true asset? What if your property could put money in your pocket instead of taking it out?

That’s the shift from being a homeowner to being a real estate investor.

Investment properties generate income. Rental properties can produce positive cash flow every month. The rent check covers the mortgage, taxes, insurance, and maintenance: with money left over for you.

House hacking changes the game. Live in one unit and rent out the others. Your tenants help pay your mortgage. Suddenly, your housing costs drop dramatically.

Short-term rentals create opportunities. Platforms like Airbnb let you rent out a spare room or entire property. The income can be substantial in the right markets.

Real estate appreciation still happens. Investment properties appreciate just like primary residences. You’re building equity while generating income.

The key difference? Investment real estate puts money in your pocket. That’s a true asset by any definition.

How to Think About Your Home

Stop thinking about your home as just a place to live. Start thinking about it as a financial tool.

Your primary residence serves important purposes. It provides shelter. It offers stability. It gives you control over your living environment. These things have value even if they don’t show up on a profit and loss statement.

But don’t confuse emotional value with financial value. Don’t assume that because you love your home, it’s automatically a great investment.

Ask yourself these questions:

- How much equity am I building each year?

- What’s the total cost of ownership including all expenses?

- Could I generate more wealth by investing that money elsewhere?

- Am I house-poor, with too much money tied up in my home?

- Would I be better off renting and investing the difference?

These aren’t easy questions. But they’re important questions.

The Smart Approach to Real Estate

Here’s what smart real estate decisions look like:

Understand your total housing costs. Calculate everything. Every expense. Every dollar going out. Know the real number.

Build equity strategically. Make extra principal payments if it makes sense. Refinance when rates drop. Don’t just follow the standard payment schedule blindly.

Consider the opportunity cost. Every dollar in your home is a dollar not invested elsewhere. Is your home equity earning its keep?

Think long-term. Real estate is a marathon, not a sprint. Short-term fluctuations don’t matter if you’re holding for decades.

Explore investment opportunities. Once you understand your primary residence, start learning about investment properties. The rules are different and the potential is huge.

Making Real Estate Work for You

The goal isn’t to avoid homeownership. The goal is to make intentional decisions about real estate.

Some people should absolutely buy homes. Others should rent and invest elsewhere. There’s no one-size-fits-all answer.

What matters is understanding the full picture. Your home is both an asset and a liability. It builds wealth and costs money. Both things are true at the same time.

The people who win with real estate are the people who understand this balance. They make smart decisions. They don’t follow conventional wisdom blindly. They think critically about every dollar.

Ready to Make Smarter Real Estate Decisions?

Real estate can be confusing. There’s a lot of noise out there. Everyone has an opinion about whether you should buy or rent, where to invest, and how to build wealth.

That’s where my 3-Step Process comes in.

Step 1: Assess your current situation. Where are you now? What are your goals? What’s your risk tolerance? We look at the whole picture, not just one piece.

Step 2: Create a clear plan. No guesswork. No following trends. Just a straightforward plan based on your specific situation and goals.

Step 3: Take action with support. Knowledge without action doesn’t change anything. I help you implement your plan and stay on track.

This process works for real estate decisions, insurance questions, investment strategies, and career growth. It’s simple. It’s practical. It works.

Want to stop guessing about your real estate decisions? Ready to get clear on whether your home is helping or hurting your financial future?

Let’s talk. Book a consultation and we’ll walk through your situation together. No pressure. No sales pitch. Just honest conversation about your real estate and financial goals.

Your home should work for you, not against you. Let’s make sure it does.